Understanding Indexed Products

The basics of indexed products

In recent years there has been a proliferation of new products utilizing various indexing strategies. Many promise the benefits of a particular financial index without its unsavory downsides. This could be an oversimplification of how these instruments work. In this edition of Financial Planning Insights we’ll address some common questions related to indexed products and help you become a better-informed consumer along the way.

What are indexed products?

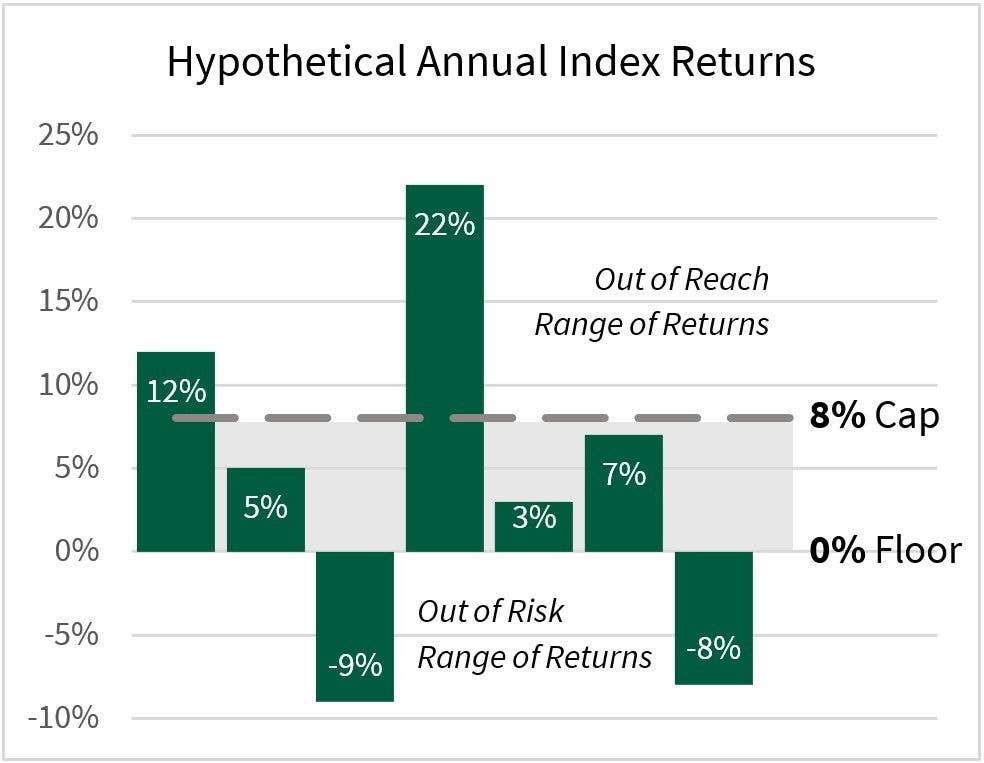

Indexed products are financial tools whose growth is tied to a market index, like the S&P 500®. The S&P 500® is one of the most widely recognized benchmarks for the U.S. stock market. Unlike direct investments, these indexed products don’t actually invest in the stock market. Instead, they use the index’s performance as a guide to calculate the performance in your indexed product. By following this method, the indexed product allows you to benefit from a portion of potential market upswings without risking market losses during downturns. This is thanks to guard rails on the product that cap how much you can earn but also limit how much you can lose due to market performance.

Why do people choose indexed products?

Many people are drawn to indexed products because they offer a balance of growth potential and downside protection. For example, an Indexed Universal Life (IUL) policy allows cash value to grow inside your permanent life insurance policy based on index performance, but it won’t lose value due to market drops. This appeals to people who want more growth than traditional fixed products but less risk than placing their money directly into the stock market.

How Do Indexed Universal Life (IUL) Policies Work?

IUL is a type of permanent life insurance that offers flexible premiums and adjustable death benefits. Part of the premium goes toward insurance costs, and the rest builds cash value. That cash value earns interest based on a chosen index and interest crediting formula. It is important to note, the credited interest is subject to a cap that limits the upside potential, and a floor that protects it from market declines. This means it grows when the market does well but won’t shrink just because the market performs poorly. This makes IUL a strategic tool for long-term financial planning, especially for those seeking tax-advantaged growth along with their life insurance needs.

What are the limitations and misconceptions?

While indexed products offer upside potential, they don’t capture all market gains. Caps limit how much interest can be credited, and fees or policy charges can reduce overall returns. Additionally, indexed products do not receive dividends paid by the companies in the index they track, which will also reduce returns relative to the performance of the associated index. Also, illustrations used to show future performance can be misleading if not properly understood. In the case of an IUL policy, there are various types of internal policy expenses, such as cost of insurance charges, which will continue to offset growth within the policy, regardless of how large the cash value may become over time. Typically, returns are credited to a policy with far less frequency than one may be used to with more traditional annuity or life insurance products. In some cases, crediting returns may only occur once a year.

Understanding these nuances is key to setting realistic expectations.

Who Are indexed products right for?

Indexed products may be a good fit for individuals who want growth with protection. They may be suitable for people who feel the market is too risky but want more growth potential than just a savings account. While the range of outcomes is more predictable than a typical portfolio of investments that fluctuate with market performance, they will still have less predictability than traditional fixed annuity or life insurance products. A financial advisor can help you analyze indexed products and whether they may be a good fit for your financial goals.

Looking for help navigating your future?

Set up a meeting with your local rep to review your current policies and make sure they're up to date. We pulled together some less obvious reasons to adjust your coverage.

This information is not intended as and should not be construed to provide tax or legal advice. It is intended as an educational starting point to help you better understand the covered topic. COUNTRY Trust Bank® and its employees do not provide tax advice, nor should you use the information here as a call to action for your personal tax situation. This information may omit some important aspects of tax or legal conditions you may face, which is why you should seek out the advice of qualified tax or legal professionals of your own choosing.

COUNTRY Trust Bank® Financial Planning Consultants

Bryan Daniels, CFP®, MPAS®, ChFC®, CLU®, AFFP®, AWMA®, ADPA®, CMFC®

Nick Erwin, CFP®, BFA, ChFC®, CLU®, AFFP®

Scott Jensen, CFP®, ChFC®, CLU®, RICP®, AFFP®

Lorraine Zenge, AFFP®

Life insurance policies issued by COUNTRY Life Insurance Company® and COUNTRY Investors Life Assurance Company®, Bloomington, Illinois.

Registered broker/dealer offering securities products: COUNTRY® Capital Management Company, 1711 General Electric Rd, PO Box 2222, Bloomington, IL 61702-2222, 1-866-551-0060. Member FINRA.

The S&P 500® (the “Index) is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”).

NOT FDIC-INSURED

May lose value

No bank guarantee

Investment management, retirement, trust and planning services provided by COUNTRY Trust Bank®.

COUNTRY Financial® is a family of affiliated companies (collectively, COUNTRY) located in Bloomington, IL. Learn more about who we are.