Optimizing Social Security Benefits

All of us know someone who suddenly decided to retire one day and then raced to the Social Security office the next day to claim their benefits. We hope that the new retirees have enough income and other resources to support themselves in their retirement. However, most of us know that it is better to head into retirement with a financial plan in place, and that the financial plan should include a well thought out decision about when to claim Social Security benefits.

Let’s look at some of the considerations surrounding claiming your Social Security retirement benefits.

Full retirement age – permanent reduction for claiming early

You will qualify for Social Security retirement benefits if you are fully insured, which means that you have earned forty credits, usually by working ten years in covered employment. If you do not have enough Social Security credits to qualify for benefits, you may be able to receive benefits on your spouse's record in the form of spousal benefits or survivor benefits. It is also important to understand that retirement benefits will be permanently reduced if you start your benefit prior to full retirement age (FRA). Full retirement age is based on the insured worker’s year of birth. The reduction of benefits, based on claiming at age 62, is shown in the chart1 below:

| Year of birth | Full retirement age | Reduction at age 62 |

|---|---|---|

| 1943-1954 | 66 | 25% |

| 1955 | 66 and 2 months | 25.83% |

| 1956 | 66 and 4 months | 26.67% |

| 1957 | 66 and 6 months | 27.50% |

| 1958 | 66 and 8 months | 28.33% |

| 1959 | 66 and 10 months | 29.17% |

| 1960 and later | 67 | 30% |

Early retirement sounds ideal. However, many Americans are forced into early retirement due to health issues, a sudden job loss, or to care for a loved one. Many early retirees claim their Social Security benefits before full retirement age to help cover living expenses or medical bills. However, claiming Social Security benefits early will permanently lower the monthly benefit amount, as well as their spouse’s spousal benefits. Moreover, claiming Social Security benefits early will lower a spouse's survivor benefits permanently, if claimed.

Next, you should be aware that there is a limit on how much you can earn and still receive your full Social Security retirement benefits while working. Your benefits will be reduced depending on your age. First, if you have not reached full retirement age, your benefits will be reduced by $1 for every $2 earned over the retirement earnings limit ($22,320 in 2024). Second, the calendar year you turn your full retirement age, a higher earnings limit is applied ($59,520 in 2024). However, your benefits will be reduced by $1 for every $3 you earn over the earnings limit. If you retire at mid-year and have already earned more than the retirement earnings limit, you can get a full Social Security payment for any whole month that you are retired (monthly earnings are $1,860 or less).2

If you are planning to work and are under your full retirement age, you should report your expected earnings and changes to the Social Security Administration, so you know specifically how these rules affect your benefits. Social Security will then calculate the effect of your earnings on your benefits and adjust or suspend your benefits until you cover what you owe. Failure to report your expected earnings may result in an unexpected repayment and penalties owed back to Social Security. All is not lost though, as Social Security will repay the benefits withheld because of the retirement earnings test once you reach your full retirement age by adding money back to your monthly benefit.

Claiming after full retirement age - Delayed Retirement Credits (DRCs)

We just covered the reduction of benefits that occurs for taking Social Security benefits prior to full retirement age. On the flipside, Social Security retirement benefits are increased by two-thirds of one percent for each month that you delay starting your benefits beyond full retirement age. The benefit increase, known as delayed retirement credits (DRCs) stops when you reach age 70.3 This is equivalent to an 8% annual increase, or 24% if your full retirement age is 67, and you wait until age 70, the latest age to claim your benefits. The delayed retirement credit increase is a simple interest increase and not compounded. Finally, remember delayed retirement credits stop accruing at 70, so delaying Social Security benefits beyond then has little to no benefit (even if you are still working).

When to claim – factors to consider

Early retirement reductions in benefits, as well as delayed retirement credits are intended to be “actuarially fair,” which means that the average person would receive the same amount of lifetime benefits, regardless of the age of when benefits are claimed.4 While there are many “Social Security break-even calculators” that estimate how long it takes for cumulative benefits begun at a later age to equal or “break-even” with benefits begun at an earlier age, no one has a crystal ball that allows them to know the exact right time to take their benefits. Let’s look at some other factors that may help you make a thoughtful decision about when to claim your benefits.

First, consider your personal health and family history of longevity. Excellent health and longer than average life expectancy points toward waiting to claim your benefits at an older age, while sub-par health points to claiming your benefits at a younger age.

However, since living longer may pose a greater risk to your retirement plan than dying sooner in terms of potentially depleting your retirement resources, it may be advisable to project a longer life expectancy. Also, for a married couple, if at least one spouse has an average outlook for longevity, the higher earner may want to delay, thereby creating a higher survivor benefit for their spouse should they predecease their spouse.

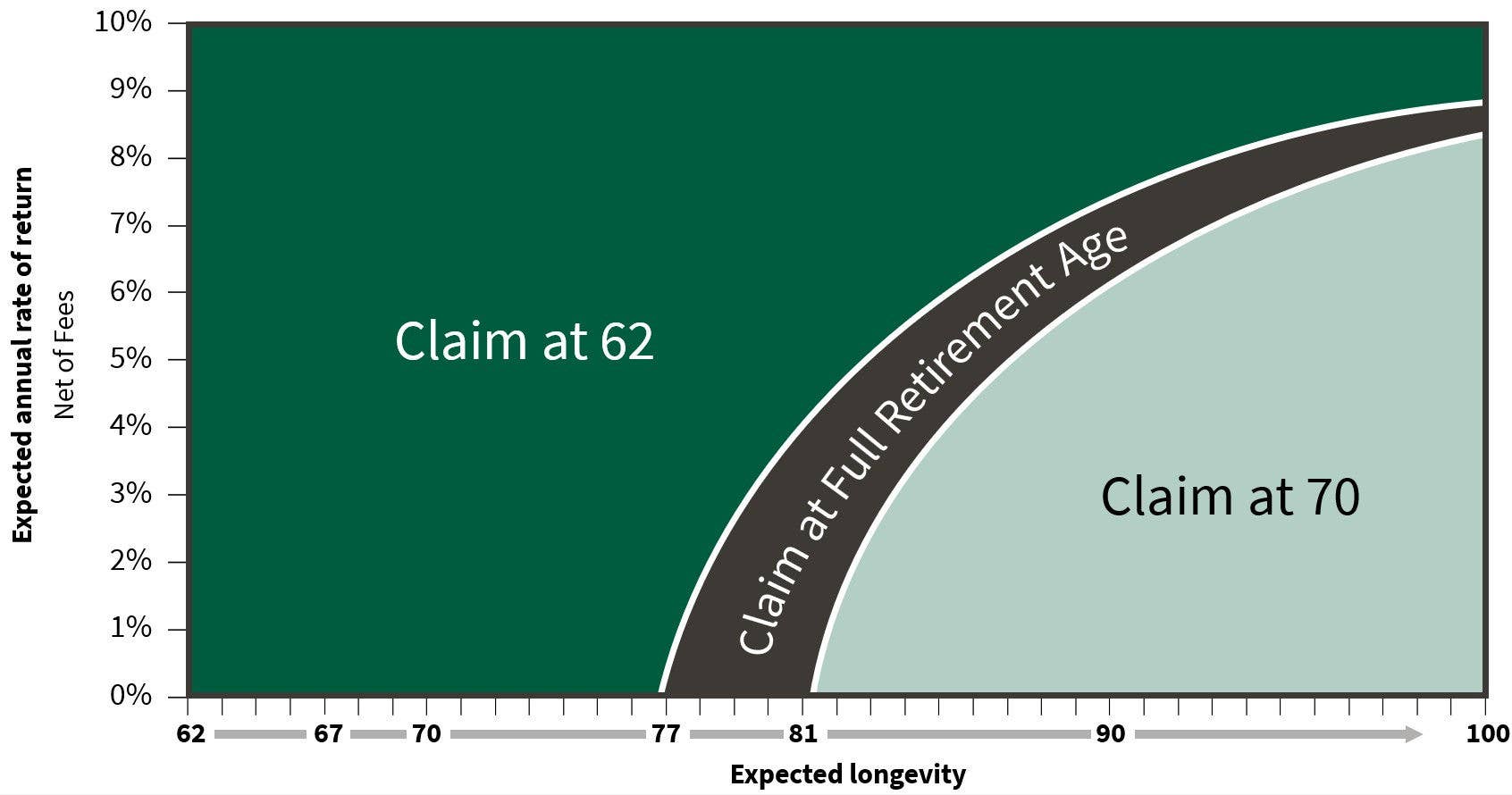

Next, review the impact of portfolio returns and inflation on your decision of when to claim your benefits. Higher periods of inflation result in a greater cost of living adjustment (COLA) on Social Security benefits. Lower returns in your investment portfolio and higher inflation point toward delaying claiming your benefits, while higher returns in your investment portfolio and lower inflation point toward claiming of your benefits earlier.

The following chart from J.P. Morgan’s Guide to Retirement illustrates the inverse relationship of expected longevity and portfolio returns on the highest cumulative expected lifetime benefits:

If you are considering delaying claiming your benefits, remember that you may need to depend more on withdrawals from pre-tax retirement accounts, such as IRAs and 401(k)s, which will then reduce future required minimum distributions. Also, if considering Roth IRA conversions as part of your retirement plan, taxable income could increase during the tax years of conversion depending on the circumstances of your individual tax situation. Delaying your benefits could help reduce taxable income and therefore reduce income tax paid during these years of Roth conversion.

If you do choose to delay claiming your benefits, it is important to have a plan to accommodate your retirement spending needs. Taking large withdrawals from accounts with substantial allocations in equities may not be desirable in a down market. Talk to your Financial Advisor about other alternatives that may help you bridge the gap until your Social Security payments begin. Alternatives might include:

- building your cash reserves to create a bucket of assets to draw from during a down market,

- using a period certain annuity to create an income stream to cover the gap until payments begin,

- taking a loan from the cash value of life insurance that you own, and

- using a reverse mortgage line of credit to supplement your retirement in a down market.

Changing your mind about when to claim your benefits

Of course, if you’ve decided to delay claiming your benefits and then decide you want to start receiving them, you can change your mind at any time. However, if you’ve already started taking your benefits and change your mind, Social Security does offer a “do-over” that is only available once during your lifetime and must be done within 12 months of starting your benefits. In addition, you must repay all the benefits that you have received, as well as deductions from your checks, such as Medicare premiums or taxes. Of course, it is better to avoid the “do-over” by good planning regarding the claiming decision.

Seek the help of a financial advisor

The decision about when to claim your Social Security benefits is one of the most important aspects of your retirement plan. Your Financial Advisor can assist you with understanding how various claiming strategies affect your retirement plan. You’ve worked hard for your Social Security benefits, and the benefits can now work for you.

Looking for help navigating your future?

Set up a meeting with your local rep to review your current policies and make sure they're up to date. We pulled together some less obvious reasons to adjust your coverage.

COUNTRY Financial® is a family of affiliated companies (collectively, COUNTRY) located in Bloomington, IL. Learn more about who we are.

1 ssa.gov/benefits/retirement/planner/agereduction.html.

2faq.ssa.gov/en-us/Topic/article/KA-01921.

3ssa.gov/benefits/retirement/planner/delayret.html.

5Assumes the same individual, born in 1962, retires at the end of age 61 and claims at 62 & 1 month, 67 and 70, respectively. Benefits are assumed to increase each year based on the Social Security Administration 2023 OASDI Trustee’s Report intermediate estimates (annual benefit increase of 2.4% in 2025 and thereafter). Analysis is based on a maximum earner (all earnings profiles yield similar results). Expected rate of return is deterministic, in nominal terms, and net of fees. Source (chart): Social Security Administration, J.P. Morgan Asset Management. Source (longevity): Social Security Administration 2023 OASDI Trustees Report

This material is provided for informational purposes only and should not be used or construed as investment advice or a recommendation of any security, sector, or investment strategy. This information is not intended as and should not be construed to provide tax or legal advice. It is intended as an educational starting point to help you better understand an array of common tax-related aspects. COUNTRY Trust Bank employees and COUNTRY Trust Bank Financial Advisors do not provide tax advice. This information may omit some important aspects of tax or legal conditions you may face. Please consult the tax or legal counsel of your choice regarding your personal circumstances.

COUNTRY Trust Bank® Financial Planning Consultants

Bryan Daniels, CFP®, MPAS®, ChFC®, CLU®, AFFP®, AWMA®, ADPA®, CMFC®

Nick Erwin, CFP®, BFA, ChFC®, CLU®, AFFP®

Scott Jensen, CFP®, ChFC®, CLU®, RICP®, AFFP®

Lorraine Zenge, AFFP®

NOT FDIC-INSURED

May lose value

No bank guarantee

Investment management, retirement, trust and planning services provided by COUNTRY Trust Bank®.